For decades, paying for higher education often relied on a simple, if risky, math equation: whatever the college charged, federal PLUS loans would cover.

Because Parent PLUS and Graduate PLUS loans allowed families to borrow up to the full Cost of Attendance (COA), the federal government effectively issued a blank check to bridge the gap between financial aid and high tuition costs. That era is officially coming to an end.

In light of the One Big Beautiful Bill Act (OBBBA), federal borrowing is shifting from the traditional “cost of attendance” model to a strict “fixed cap” model. Starting July 1, 2026, new limits and the outright elimination of key loan programs will fundamentally change how families fund undergraduate and graduate degrees.

If you are planning for college or graduate school, here is exactly how these sweeping changes will impact your wallet.

The New Federal Borrowing Limits: A Closer Look

The OBBBA restructuring targets three major categories of federal borrowing. Here is the breakdown of the new caps and timelines.

1. Parent PLUS Loans

For decades, parents could borrow up to the full cost of attendance (COA). That era is ending for new borrowers.

- Annual Cap: $20,000 per student per year.

- Lifetime Cap: $65,000 per dependent student.

- The “Penalty” Impact: If a student attends an expensive private or out-of-state school with a COA of $60,000 per year, and federal aid covers only $30,000, the parent can no longer bridge the entire $30,000 gap with a PLUS loan. They are capped at $20,000, leaving a $10,000 shortfall that must be covered by savings or private loans.

- Legacy Rule: If you are an existing Parent PLUS borrower (meaning you had a loan disbursed before July 1, 2026), you can generally continue borrowing under the old “up to COA” rules for up to three years or until the student graduates.

2. Graduate PLUS Loans

This is the most significant change: Graduate PLUS loans are being eliminated for new borrowers.

- Effective Date: July 1, 2026.

- Replacement: There is no direct “PLUS” replacement. Instead, the government has increased the limits on standard Direct Unsubsidized Loans (see below), but for many students, these new limits will be lower than the total cost of their degree.

- Legacy Rule: If you already have a Grad PLUS loan disbursed before July 1, 2026, you may be able to continue borrowing under the old rules until you finish your current program (typically through June 2029).

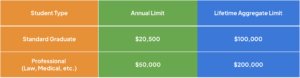

3. Graduate & Professional Direct Loans

Since Grad PLUS is disappearing, the government adjusted the limits on Unsubsidized Direct Loans. The limits now depend on whether you are in a “Standard” graduate program (MA, MS, PhD) or a “Professional” program (MD, JD, DDS).

Note: The aggregate limits include all graduate borrowing but do not include what you borrowed as an undergraduate. However, there is a “Hard Ceiling” of $257,500 for total combined federal debt (Undergrad + Grad).

Closing the Funding Gap Going Forward

The ultimate consequence of the OBBBA is the creation of an immediate, structural funding gap. By removing the federal safety net that automatically expanded to match rising tuition, the government is forcing a massive shift in how higher education is financed.

What does this mean for future students and parents?

-

An Inevitable Push Toward Private Lenders: If your chosen school’s tuition and living expenses exceed these new federal caps, you will have to turn to private banks.

-

Loss of Federal Protections: This shift is highly consequential. Private loans rarely offer the flexible, safety-net protections built into the federal system, such as income-driven repayment options (like the RAP plan) or public service loan forgiveness.

-

A Shift in College Choice: Families will need to be much more price-sensitive. Choosing an in-state public university or a school offering robust institutional merit aid will no longer just be a smart financial decision—for many, it will be the only viable choice.

The rules of the game have changed. As July 1, 2026, approaches, it is more critical than ever to map out a college funding strategy early, calculate your potential shortfalls, and look beyond federal loans to bridge the gap.

We are in a whole new world of paying for college, so it’s now more important than ever to know each and every method, trick, and loophole you can use to not only save for college, but get the most free money for college, as well. If you’re ready to learn from an expert, please schedule time with me, and we’ll create an action plan.