Key Takeaways:

- The SAVE plan’s end changes how borrowers approach federal student loan repayment and forgiveness options.

- The new RAP system may affect monthly payments, repayment timelines, and long-term costs.

- Understanding your options now can help you make smarter student loan decisions.

The landscape of federal student loan repayment has been completely rewritten. If you’ve been keeping an eye on the news regarding the Saving on a Valuable Education (SAVE) plan, the biggest takeaway is this: it is officially gone, terminated by a federal appeals court order.

In its place, a massive legislative overhaul established by the One Big Beautiful Bill Act (OBBBA) is taking the reins, with core changes set to drop on July 1, 2026. For the 7.5 million borrowers left stranded by the death of SAVE, the government has accelerated the timeline. You won’t have until 2028 to figure out your next moves—you have a strict 90-day window to manually choose a new plan, or you’ll be automatically defaulted into a standard payment schedule.

Here is a breakdown of the new system, what it replaces, and why some parts feel less like assistance and more like a penalty.

Out with SAVE, In with RAP

The exceptionally generous SAVE plan is being replaced by the Repayment Assistance Plan (RAP). Going forward, RAP will act as the primary Income-Driven Repayment (IDR) framework.

Until recently, managing federal student debt meant choosing from a complex menu of Income-Driven Repayment (IDR) options, including Pay As You Earn (PAYE), Income-Contingent Repayment (ICR), Income-Based Repayment (IBR), and the short-lived SAVE plan.

But now, for anyone taking out new loans on or after July 1, 2026, your only options will be RAP or the new Tiered Standard Plan.

The Repayment Assistance Plan (RAP)

The Repayment Assistance Plan (RAP) is the newly minted flagship IDR plan. For anyone borrowing on or after July 1, 2026, RAP will be the only income-driven option available.

When to Consider RAP

RAP is a strong candidate if your total debt is high relative to your income. It offers two highly beneficial features designed to stop the debt from spiraling:

- No Growing Balances: If your calculated monthly payment is too small to cover the interest building up on your loan, the government waives the rest. Your balance will never suffer from negative amortization.

- Principal Subsidy: If your on-time RAP payment reduces your principal balance by less than $50 in a month, the government steps in to pay the difference, guaranteeing you chip away at the actual debt every month.

Unlike older IDR plans, RAP has no upper payment cap. If your income skyrockets, your mandatory payment will soar past what you would have paid on a standard plan. Furthermore, RAP extends the loan forgiveness timeline to a 30-year track (up from 20 or 25 years). Lastly, starting July 1, 2027, new loans under this system lose access to Economic Hardship and Unemployment Deferments entirely.

How RAP Payments Are Determined

Instead of using discretionary income, RAP calculates your bill using a flat percentage of your Adjusted Gross Income (AGI) on a sliding scale.

The biggest shift is how your payment is calculated. While old IDR plans looked at “discretionary income” (what you have left over after basic living expenses), RAP shifts the math to your Adjusted Gross Income (AGI) on a sliding percentage scale:

-

Under $10,000: A flat $10 per month.

-

$10,001 to $20,000: 1% of your AGI.

-

The Scale Moves Up: The percentage grows by 1% for every additional $10,000 you earn.

-

$100,001 and up: A flat 10% of your total AGI.

Note: Your calculated monthly payment is discounted by $50 for each dependent child claimed on your tax return, though the total bill cannot drop below the $10 monthly floor.

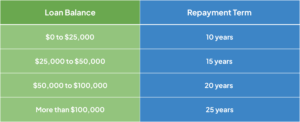

The Tiered Standard Repayment Plan

The historical Standard Repayment Plan enforced a rigid 10-year timeline for everyone. Starting July 1, 2026, the new Tiered Standard Repayment Plan replaces it. Under this framework, your monthly payment is fixed, but the length of your repayment term scales dynamically based on your total initial loan balance.

For standard non-IDR repayment, the traditional 10-year fixed plan is also getting reshaped for new timelines. A new Tiered Standard Repayment Plan links your timeline directly to how much you owe:

Case Studies: The $100,000 Debt Dilemma

To see how these two new plans clash in the real world, let’s look at three different single borrowers who each owe $100,000 in federal loans (at a 6.4% interest rate).

Because their debt exceeds $100,000, their baseline Tiered Standard Plan requires a fixed payment of $669 per month for 25 years, regardless of their salary. Here is how their bills change if they choose RAP:

1. The Entry-Level Professional ($50,000 AGI)

- RAP Bracket: 4% tier

- RAP Monthly Payment: ($50,000 × 0.04) ÷ 12 = $166.67 per month

- The Verdict: RAP is an easy win here. It saves this borrower over $500 a month compared to the Standard Plan, protects their monthly cash flow, and unlocks the government interest subsidies.

2. The Mid-Career Earner ($100,000 AGI)

- RAP Bracket: 9% tier

- RAP Monthly Payment: ($100,000 × 0.09) ÷ 12 = $750.00 per month

- The Verdict: This is where the lack of a payment cap hurts. Because this borrower earns a healthy salary, RAP actually costs them $81 more per month than the Tiered Standard Plan ($750 vs. $669). They should steer clear of RAP and stick to the Standard Plan.

3. The High Earner ($250,000 AGI)

- RAP Bracket: 10% tier

- RAP Monthly Payment: ($250,000 × 0.10) ÷ 12 = $2,083.33 per month

- The Verdict: RAP acts as a massive financial penalty for high earners, demanding more than triple the Standard Plan amount. This borrower should select the Tiered Standard Plan to lock in the lower mandatory floor ($669) and then aggressively pay down principal on their own terms.

How the New System “Penalizes” Borrowers

While the RAP plan introduces a few technical patches, the financial reality is much more restrictive and expensive for the average working household.

-

Massive Payment Spikes: Because RAP calculates your debt against your base AGI rather than your discretionary income, your monthly bills are going to look wildly different. Under the old SAVE structure, a family of four earning $81,000 might have paid a modest $36 a month. Under RAP, that same family will likely see their monthly bill skyrocket to roughly $440.

-

The 30-Year Timeline: Most classic IDR plans capped your path to forgiveness at 20 or 25 years. RAP pushes the finish line out to 30 years, turning student debt into a lifelong working companion for many.

-

The Stripping of Safety Nets: Beginning July 1, 2027, newly disbursed loans will completely lose eligibility for Economic Hardship or Unemployment Deferments. The government’s justification is that the low-income RAP tiers ($10/month) eliminate the need to pause payments, but it completely removes the security blanket of a true $0 pause during unexpected life crises.

-

The Legacy Trap: If you have older loans, you can safely stick to legacy plans like Income-Based Repayment (IBR) for now. However, if you consolidate your loans or take out a new loan after July 1, 2026, you run the risk of being forced into the RAP system, forfeiting your shorter 20-year forgiveness tracks. Furthermore, the OBBBA will completely phase out alternative options like PAYE and ICR by 2028.

Is There a Silver Lining?

It’s not entirely bleak; lawmakers did manage to remedy one of the most widely despised psychological burdens of federal student loans.

-

No More Balances Growing in Reverse: Under RAP, if your calculated monthly payment isn’t enough to cover the interest that accrues that month, the government waives the rest. This stops negative amortization, meaning your balance won’t balloon while you’re actively making payments.

-

The Principal Subsidy: If you make your RAP payments on time, the government will credit up to $50 towards your principal balance every single month.

-

PSLF Remains Untouched: The Public Service Loan Forgiveness program is still active. RAP payments fully count toward your 120 qualifying payments required for tax-free forgiveness after 10 years of public service.

Summary: Old vs. New Frameworks

The July 1, 2026 Crossroad: Opportunities for Existing Loans

If you currently hold existing student loans, you are grandfathered into a critical window of opportunity—but you have to watch your step.

- Preserving Legacy Plans: If you don’t take out any new loans, you can choose to remain on your existing standard tracks or select legacy IDR plans like IBR, PAYE, or ICR. However, be aware that the OBBBA officially phases out PAYE and ICR by July 1, 2028.

- The “New Loan” Trigger: The moment you take out a new federal loan or initiate a new Direct Loan Consolidation on or after July 1, 2026, the door to the past slams shut. All of your loans will instantly shift into the new system.

- The Parent PLUS Urgency: Parent PLUS loans are entirely barred from the new income-driven relief system. If you are a parent borrower needing an income-driven track, you must consolidate your loans before July 1, 2026 to secure access to the legacy ICR plan before it sunsets.

What Should You Do Right Now?

If you are currently sitting on the now-defunct SAVE plan, your immediate priority is to log into your Federal Student Aid account at studentaid.gov check your loan servicer, and map out your next 90 days. Run your numbers through a loan simulator to weigh the long-term impact of switching to the RAP plan versus older legacy options like IBR. Stopping interest growth is great, but make sure it’s worth adding 5 to 10 years to your life timeline before you lock yourself into the new system.

If you have any questions about these new changes to student loans, please schedule time with me so we can talk ASAP.