There has been a lot of news in recent months about the ACA enhanced subsidies expiring at the end of the year. Extending the beefed-up subsidies has been at the center of several battles on Capitol Hill in recent months, including the longest government shutdown in the nation’s history.

The Future of Health Insurance Subsidies

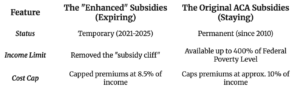

If you’ve seen the myriad headlines about health insurance subsidies “disappearing,” take a deep breath. The help isn’t going away — it’s just shifting back to its original settings. The extra “enhanced” subsidies introduced during the 2021 relief package are set to expire, but the foundational support from the original 2010 Affordable Care Act remains firmly in place.

What Stays The Same:

- Financial Protection: Low income families are still protected from high premiums. Original subsidies will continue to cap monthly payments.

- Income Caps: If your household income is under 400% of the federal poverty level (roughly $62,600 for an individual or $128,600 for a family of four), you still qualify for help.

- The 10% Rule: For most, monthly payments for a standard plan will still be limited to about 10% of your household income.

What’s Actually Changing in 2026?

Summary of the “Subsidized vs. Unsubsidized” Shift

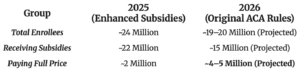

This may come as a shock to you, but in 2025 only about 1 in 5 people purchased health insurance through the ACA Marketplace without any subsidy or tax credits. That means that roughly 80% got some form of subsidy.

Under the original ACA Subsidies kicking back in for 2026, approximately 2 million to 3 million people currently receiving subsidies are expected to lose them entirely because their income exceeds the 400% FPL threshold. You are either in or you’re out, based on the subsidy cliff.

Premiums Are Going Up Anyway

2026 will bring notable premium increases regardless of the subsidy you may qualify for. Insurers have cited rising drug costs (specifically GLP-1s) and more people utilizing insurance. Enrollment in the ACA Marketplace has nearly doubled since 2021 when the enhanced subsidies kicked in, topping 23 million in 2025.

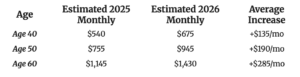

For those of us on an employer plan or on Medicare, you may have some sticker shock. The premium estimates below are for one person per month. This should stand as a good reminder of how much your employer subsidizes your health insurance premium.

On average, the “sticker price” premiums are projected to rise by approximately 20% to 26% nationally to account for rising drug costs and the “death spiral” fear — the idea that healthy people will leave the market when subsidies expire, leaving a costlier pool of sick people behind.

Below is an estimate of how these gross monthly premiums look across key age brackets for an individual standard Silver-tier plan:

Note: These are national averages. Your specific premium may vary significantly based on your state and the specific plan you choose during Open Enrollment.

What Does All of This Mean For My Family?

For a family of five living in Dublin, Ohio, earning $155,000, hitting the 2026 “Subsidy Cliff” is a significant financial event. Because the enhanced subsidies are expiring, families earning more than approximately $150,600 will be responsible for the full market price of their insurance.

Based on 2026 premium projections from the KFF and Urban Institute, here is what a family in that situation can expect to pay on average.

Estimated Premiums (Unsubsidized)

For a family of 5 (two 45-year-old parents and three children under 17), the estimated national average for a Silver “Benchmark” Plan in 2026 is:

- Estimated Monthly Total: $2,600 – $3,400

- Estimated Annual Total: $31,200 – $40,800

Monthly & Annual Take-Home Pay (2026 Estimate)

For a family of five filing Married Filing Jointly with three children under 17:

Highway To The “Danger Zone”

At $155,000, you are roughly $4,400 over the subsidy threshold. In a “cliff” year like 2026, those extra few thousand dollars in earnings could actually make you poorer in terms of spending power.

- Your Take-Home Pay: $10,521 / month

- Market Price Premium (Avg): ~$3,000 / month

- Remaining for all other bills: $7,521 / month

If your income were just $5,000 lower ($150,000), you would likely qualify for a subsidy that caps your health insurance at about $1,250/month.

The Danger Zone: By earning an extra $5,000 in salary, you lose roughly $21,000 a year in health insurance subsidies. This effectively gives you a “negative” raise of $16,000 for the year.

This is where “financial planning” kicks in. Your eligibility for subsidies is based on your Modified Adjusted Gross Income (MAGI), not your total salary.

By using “above-the-line” deductions, you can lower your MAGI and pull your household back under the $150,600 cliff. This is essentially getting a massive “discount” on health insurance for the price of paying yourself first.

How to “Hide” $5,000 to Save $21,000

If you earn $155,000, you are exactly $4,400 over the cliff. To get back to safety, you simply need to move that money into specific tax-advantaged accounts.

1. The Traditional 401(k) (The Easiest Way)

- 2026 Limit: $24,500 per person.

- The Move: If one or both parents contribute a total of just $5,000 to their employer’s traditional (pre-tax) 401(k), your MAGI drops to $150,000.

- Result: You are now under the 400% FPL line. You qualify for the subsidy again.

2. The Health Savings Account (HSA)

- 2026 Limit: $8,750 for family coverage.

- The Move: If you choose a “Bronze” or “HSA-Eligible Silver” plan, you can put money into an HSA.

- Result: Like the 401(k), HSA contributions are deducted before your MAGI is calculated.

The “Cliff-Jumper” Comparison

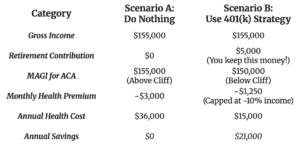

Here is what happens to your family’s finances if you earn $155,000 and decide to contribute $5,000 to a 401(k) to avoid the cliff:

The Outcome: In Scenario B, you have $16,000 more in your pocket at the end of the year than in Scenario A—PLUS you have an extra $5,000 growing in your retirement account.

Critical Warnings for 2026

- The “All-or-Nothing” Rule: Unlike taxes, which are tiered, the subsidy cliff is a tripwire. If you earn $150,601, you lose all $21,000 of the subsidy. There is no partial credit for being “close.”

- Standard Deduction Doesn’t Count: Be careful! The $32,200 standard deduction lowers your taxable income, but it does not lower your MAGI for ACA purposes. You must use 401(k), HSA, or Traditional IRA contributions to move the needle.

- Avoid “Roth” for this Strategy: Contributions to a Roth 401(k) or Roth IRA do not lower your MAGI. You must use the “Traditional” (pre-tax) versions to get the health insurance discount.

Where The Rubber Hits the Road

Our clients are often on track to achieve their goal of making work optional (AKA – Retirement) in their late 50’s and early 60s. This is largely attributed to your consistent hard work and discipline in saving for the future, complemented, of course, by the sage wisdom and guidance of your Capstone team. One of the main challenges for clients to overcome is the high cost of health insurance until you are eligible for Medicare at 65.

For a 60-year-old couple in Dublin, OH, the “Subsidy Cliff” is even steeper than it is for younger families. This is because health insurance premiums for older adults are naturally much more expensive. When you lose a subsidy at age 60, you aren’t just losing a small discount—you are losing a massive federal contribution that covers the majority of your bill.

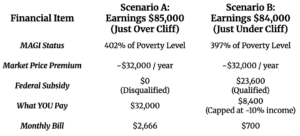

In 2026, the cliff for a household of two is projected to be $84,600.

The 2026 “Cliff” Comparison (Age 60 Couple)

Here is the math for a couple (both age 60) living in a typical market. Because of their age, the “sticker price” of their insurance is significantly higher than a younger person’s.

Why the impact is so much worse at 60

Under the original ACA rules, insurers can charge a 64-year-old up to three times more than a 21-year-old. Because of this:

- The Sticker Price is Huge: A 60-year-old couple might see a total premium of $32,000, while a 30-year-old couple might see $12,000 for the same plan.

- The Subsidy is Massive: To make that $32,000 plan “affordable” (10% of income), the government has to kick in over $23,000 a year.

- The Fall is Harder: If you earn one dollar over the $84,600 limit, you don’t just lose a small tax break—you lose that entire $23,000 government contribution. This is effectively a 27% “tax” on your total income just for earning that extra dollar.

The Dublin, OH Example: Tax vs. Health Costs

If this couple lives in Dublin, OH and earns $85,000:

- Take-Home Pay (after tax): ~$68,000

- Health Insurance Bill: $32,000

- Left for everything else: $36,000 ($3,000/month for mortgage, food, cars, utilities).

If they lower their income by just $1,000 (to $84,000) using a Traditional IRA or HSA:

- Take-Home Pay: ~$67,300

- Health Insurance Bill: $8,400

- Left for everything else: $58,900 ($4,908/month).

The Verdict: By “lowering” their income by $1,000, this couple actually increases their spendable cash by $22,900 for the year.

Strategy for Retired Couples

When you are retired and no longer have “earned income” (wages from a job), the classic strategies like contributing to a 401(k) or a Traditional IRA are off the table because they require a paycheck.

However, retirees have a different—and often more powerful—toolkit to control their Modified Adjusted Gross Income (MAGI) and stay below the $84,600 cliff.

1. Use Roth IRA

Roth IRA withdrawals are powerful for ACA planning.

- How it works: Money taken out of a Roth IRA is generally tax-free and does not count toward your MAGI.

- The Strategy: If you need $100,000 to live on but want to keep your income at $84,000 for the subsidy, you can take $84,000 from your taxable sources (like a Pension or Traditional IRA) and the remaining $16,000 from your Roth IRA. Your “income” for the ACA remains $84,000.

2. Spend “Principal,” Not “Gains”

When you sell stocks or mutual funds in a regular (taxable) brokerage account, you aren’t taxed on the whole amount—only the profit.

- How it works: If you sell $50,000 worth of stock that you originally bought for $40,000, only the $10,000 profit counts toward your MAGI. The $40,000 “basis” is invisible to the ACA.

- The Strategy: In “cliff years,” sell assets with a high cost-basis (those that haven’t grown much). This allows you to put a large amount of cash in your bank account while barely moving the needle on your MAGI.

3. The “IRA-to-HSA” One-Time Transfer

This is a little-known “ninja move” for retirees.

- How it works: Once in your lifetime, the IRS allows you to move money directly from a Traditional IRA into an HSA (up to the annual limit, which is $10,750 for a 60+ couple in 2026).

- The Strategy: Even with no earned income, this transfer counts as an “above-the-line” deduction that lowers your MAGI. While regular HSA cash contributions can be made up until the April 15 tax filing deadline, the IRA-to-HSA one-time transfer (technically called a Qualified HSA Funding Distribution or QHFD) does not. The IRS counts the transfer in the calendar year the money actually moves.

4. Tax-Loss Harvesting

If you have some “losers” in your portfolio, 2026 is the year to sell them.

- How it works: You can use investment losses to offset your investment gains.2 If your losses exceed your gains, you can deduct an additional $3,000 against your other income (like your Pension or Social Security).3

- The Strategy: Selling a bad investment to lock in a $3,000 loss can be the difference between getting a $23,000 subsidy and getting $0.

5. Delay Taking Social Security

When calculating your MAGI for the ACA, retirees often don’t realize the impact of taking social security early until it is too late.

- How it Works: Even the “non-taxable” portion of your Social Security must be added back to your MAGI for ACA purposes. You must use the gross amount of your benefit.

- The Strategy: We suggest delaying the start of your Social Security benefits until you qualify for Medicare, which is typically age 65. Although you can begin drawing Social Security as early as age 62, waiting until age 65—provided you can cover living expenses with other resources as outlined—is essential to help secure the $23,000 ACA subsidy. You will also see a permanent increase (approx. 8% each year) in your social security benefit for each year you wait to begin receiving it.

Summary

2026 Quick Reference: The “Subsidy Survival” Cheat Sheet

| Category | 2026 Limit/Threshold | Impact on ACA Subsidy (MAGI) |

| 401(k) / 403(b) Limit | $24,500 | Reduces MAGI (Traditional only) |

| Catch-up (Age 50–59 & 64+) | +$8,000 | Reduces MAGI (Unless Roth-mandated*) |

| “Super” Catch-up (Age 60–63) | +$11,250 | Reduces MAGI (Unless Roth-mandated*) |

| Family HSA Limit | $8,750 | Reduces MAGI |

| HSA Catch-up (Age 55+) | $1,000 per person | Reduces MAGI |

| Standard Deduction (MFJ) | $32,200 | NO IMPACT on MAGI |

| Standard Deduction (Single) | $16,100 | NO IMPACT on MAGI |

To keep your health insurance cheap, pull your money in this order:

- Cash/Savings: $0 impact on MAGI.

- Roth IRA: $0 impact on MAGI.

- Brokerage Sales (High Basis): Minimal impact on MAGI.

- Pensions/Traditional IRAs: 100% impact on MAGI (Use these only up to the $84,600 limit).