What Expenses Can Be Paid from a 529 Plan?

Up to this point, parents have SAVED for college and SHOPPED for college. Suddenly, you come to a momentous occasion–you have to PAY for college. Gulp! Often parents face this

Up to this point, parents have SAVED for college and SHOPPED for college. Suddenly, you come to a momentous occasion–you have to PAY for college. Gulp! Often parents face this

Part of being an informed consumer of a college education is understanding some of the tax implications of certain situations in our lives. This is of particular interest to families

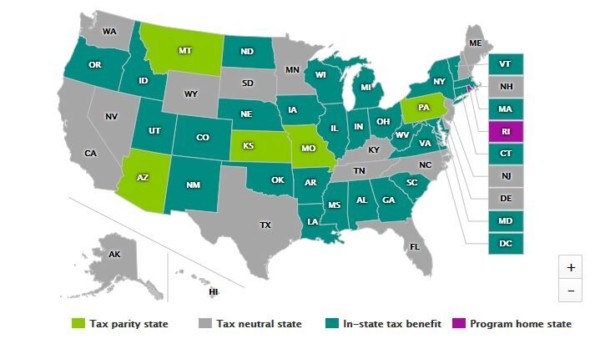

To encourage saving for college, many states in the US allow for an in-state tax deduction up to a certain amount for savings invested in that state’s 529 plan. Starting

Before the existence of 529 plans, there was the UTMA, Uniform Transfers to Minors Act. Parents and grandparents could create UTMA accounts in their child’s name, put money in them, and not only save for college (or something else) but also avoid paying the higher tax percentages of the parent. A perfect tax shelter…your children! In the 80’s, the government got wise and passed “kiddie tax” laws to remove this shelter loophole. As a result, UTMA accounts have tax implications you need to consider when choosing this savings product.

Many families recognize the value of 529 savings plans. 529 plans provide an easy way to put aside money for college that will earn interest tax-free (when used for qualified college expenses). Plus by setting up direct deposits, parents can create a deposit schedule for their plan and pretty much forget about it. However, when the time comes to make withdrawals from that plan, questions can arise.

Susan Kannenwischer, director of financial aid at Capital University, and Joe Messinger, co-founder of Capstone Wealth Partners, explain why learning a student’s Expected Family Contribution number is just the start in determining college expenses.

Check out the second post of our 5-part video series, featuring our co-founder, Joe Messinger, CFP®, and Susan Kannenwischer, Director of Financial at Capital University. In this video, Joe and Susan discuss important factors about the Free Application for Federal Student Aid, otherwise commonly known as the FAFSA.

Check out the first of our 5-part video series, featuring our co-founder, Joe Messinger, CFP®, and Susan Kannenwischer, Director of Financial at Capital University. In this first video, Joe and Susan point out the critical need to discuss college affordability as early as possible.