Key Takeaways:

- Parent PLUS borrowers have a limited window to protect their future borrowing and repayment options.

- Taking action before July 1, 2026, may help families preserve access to more flexible loan rules.

- New Parent PLUS limits could create funding gaps for families who rely on loans to pay for college.

In case you haven’t read our previous post on student loans, beginning July 1st, 2026, the student loan ecosystem is undergoing major changes, so I’ve been fielding a lot of questions from parents because one of the many changes to student loans is the new cap on the Federal Parent PLUS Loan.

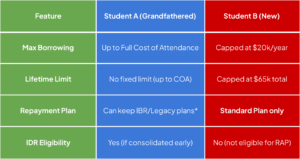

The current rules allow you to take out a Parent PLUS Loan up to the full cost of attendance, less any aid you have received. Under the One Big Beautiful Bill Act (OBBBA), Parent PLUS loans will now have an annual cap of $20,000 and a lifetime cap of $65,000 per student.

However, there is a silver lining known as the “Legacy Provision” (or grandfathering). If you take out even a tiny Parent PLUS Loan (as little as $100) before the July 1st, 2026 deadline, you can lock in the old rules for that student. This means you preserve the ability to borrow up to the full Cost of Attendance for that child for the rest of their undergraduate career.

Case Study: A Current College Freshman and a Soon-To-Be College Freshman

Last week, I spoke with a couple who have one child who is currently a college freshman, and another child who will be entering college next year in 2027, and their question was:

“If we take even a small Parent PLUS loan, can we get grandfathered into the old rules, and would that be grandfathered in for both of them or just the one that we already have in school?”

Yes, their currently enrolled student with a loan will be grandfathered into the old rules. However, since the younger student won’t be enrolled until the fall (after the July 1st deadline), they will not be grandfathered under the old rules.

If this sounds like your situation and you think you may need access to some capital (loan) to fund the last year or two of college when you have overlapping students in college, you may want to consider taking even a small amount of Parent PLUS loan before July 1st, 2026, to be grandfathered into the current rules.

While I am generally not a huge fan of Parent PLUS Loans due to their high origination fees and interest rates, having this option locked in as a backup plan is an incredibly smart safety net.

Here’s a breakdown of what each student’s situation could look like moving forward:

The Small Amount Strategy For Current Freshmen

If you take out even a $100 Parent PLUS loan for your current student before July 1, 2026, you successfully “lock in” the old rules for that specific student.

- The Benefit: You can continue to borrow up to the full Cost of Attendance (COA) for that student for up to three more years or until they graduate.

- The Catch: This applies only to the student for whom the loan was disbursed. It does not create a “blanket” grandfather status for you as a parent that extends to other children.

The Strategy for Incoming Freshmen

Because your second student is starting their program after the July 1 deadline, they are considered a “new borrower” under the OBBBA. Even if you are already a Parent PLUS borrower for their older sibling, the new limits will apply to the second child:

- Annual Cap: You will be limited to $20,000 per year for this student.

- Lifetime Cap: You can only borrow a total of $65,000 for this student’s entire undergraduate career.

- The Gap: If the college costs $50,000 per year and the student receives $10,000 in aid, you will have a $20,000 gap that cannot be covered by federal Parent PLUS loans. You would need to look at private loans or personal savings to fill it.

The Repayment Trap Warning

This is the most critical part of the new law for parents with multiple students. Taking a new loan for your second child could ruin the repayment options for your first child’s loans.

- The Rule: If you take out a “New” Parent PLUS loan (disbursed after July 1, 2026) for your second child, the law may require all of your Parent PLUS loans to be moved into the Standard 10-year Repayment Plan.

- Loss of Benefits: This means you could lose access to Income-Driven Repayment (IDR) plans or progress toward Public Service Loan Forgiveness (PSLF) for the older loans.

- The Fix: If you are pursuing PSLF or want an income-based payment, you must consolidate your existing Parent PLUS loans for the first student into a Direct Consolidation Loan before July 1, 2026.

Final Thoughts

The game is changing on July 1st, and I call this strategy the “Catch Me If You Can” window. You have to act before the deadline to protect your borrowing flexibility.

If you have a student currently enrolled in college and foresee a need for extra capital to fund their final years, taking out a small Parent PLUS loan right now is a low-risk way to keep your options open. For your younger students, start planning now for the reality of the $20,000 annual cap so you aren’t caught off guard by an unfundable financial gap down the road.

Among the most drastic changes is a new restriction on the Federal Parent PLUS Loan. If you have a child currently in college and another one entering in the near future, understanding these new rules—and how to navigate them—could save your family from a major financial gap, so if you have any questions, please do not hesitate to schedule a complimentary session with me.