In Part 1 of College Planning with Tax Strategies, we looked at tax strategies higher-income families can use, including gifting appreciated assets to your child and personal tax filings.

Today, we’re going to take a closer look at the special opportunities available to business owners. Often, a business owner will fit into what we call the high merit/low need category, meaning they earn too much to qualify for need-based financial aid. (However, their student may qualify for scholarships based on academics.)

When searching for more financial aid for college, the focus lies on the buckets below:

- Non-need merit aid offered by institutions based on GPA and test scores

- Private scholarships (not need-based)

- School selection – Schools that will award non-need-based merit aid to your child

- Test prep – Higher ACT or SAT scores could mean tens of thousands of dollars over four years

- Tax aid – Utilizing the system to your advantage

These 5 buckets will all ultimately result in a lower net cost to your family, but in today’s blog, we’ll explore bucket number five – tax aid – more in depth.

💰 Strategy 1: Hiring Your Child in Your Business

Families who own businesses need to think outside the box to realize the most savings and utilize their own student’s tax capacity.

A great option to consider is hiring your young adult to work for your business. They need to work, be documented, and on the payroll. They can keep the books, sweep the floors, take out the trash, shred documents, or whatever work your business needs. You can implement this strategy in your child’s junior or senior year of high school, but you don’t have to wait until your student is actually in high school.

Take note: your accountant will need to structure this properly for you. An accountant can be sure you are not overpaying your student, and everything is documented properly. Aside from the tax benefits, having your kids be a part of the business is an exciting way to train the next generation to continue your business.

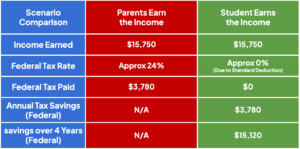

Here’s an example of how this could work, using 2025 figures:

Case Study: The Tax Scholarship (2025)

Let’s assume the base income for you, the parents, is $250,000, putting you in the 24% federal income tax bracket (Married Filing Jointly) and 5.4% state of Ohio income tax brackets.

Say you’re going to pay your student working for your business $15,750 — the 2025 Standard Deduction for single. If this $15,750 remains earned by the parents, it would result in:

- Federal Tax: $15,750 at 24% = $3,780 Tax

- State Tax: $15,750 at 5.4% = $850.50 (estimated, may vary)

- Total Tax Due: $4,630.50

Now, if you paid your student employee that $15,750 instead, the student’s 2025 Standard Deduction for a single filer is $15,750 (for earned income). This amount is below the taxable threshold, which means the student would likely have no federal tax due on this money, and the business gets a deduction for the wages paid.

This is a smart way to utilize your child’s tax capacity to realize savings that were not there before. As a family, you are mitigating taxes and maximizing cash flow.

💵 Strategy 2: Combining Wages, Gifting, and Tax Credits

Let’s take a look at an ultra-high-income family like a doctor or dentist with an income over $700,000 (a more current ultra-high bracket).

Perhaps your children want to follow in your footsteps in this career, and so you employ them in your business. What happens to the tax picture when you can gift appreciated assets to your child and hire them in your practice?

Let’s use a comparative case study, updating the numbers for the 2025 tax year.

Case Study: Comparing Tax Outcomes (2025)

This case study is a family trying to figure out the best way to pay a $25,000 college bill. We’ll show you the results for one year. The parents are Married Filing Jointly.

- Parent Pays: With the parent’s income over $700,000, they are in the 37% federal marginal income tax bracket and subject to a 23.8% long-term capital gains tax rate (20% + 3.8% Net Investment Income Tax (NIIT). The combined tax on $50,000 of income/gain is $15,200 gross federal tax per year. OUCH!

- Student Pays: By paying the student wages ($15,750, the 2025 Standard Deduction for single) and gifting appreciated assets, the student can meet the “support test” and file their own taxes. They are not subject to tax on their earned income or the capital gains from selling the gifted assets (assuming they avoid the Kiddie Tax thresholds and meet the support test). They can then claim the American Opportunity Tax Credit (AOTC) of $2,500, which the parents could not, resulting in a $1,000 refund (the maximum refundable portion of the AOTC).

In the second scenario, you avoided paying the $15,200 tax, and your child received a $1,000 refund for a total annual tax savings of $16,200 per year. Over a four-year period, the total becomes a $64,800 savings!

🎓 Strategy 3: Tuition Reimbursement Plans

One more idea to explore: tuition reimbursement plans.

These plans are a valuable employee benefit to consider if you can afford them and they suit your business and family situation. Employers benefit from smarter, more promotable employees, better retention, and more competitive recruiting when seeking new staff. However, these are not a slam dunk for every business. Make sure to do your due diligence by understanding the rules, regulations, and reporting requirements before implementing.

If your child is an employee filing their own taxes, they can apply for a tuition reimbursement plan. Businesses are eligible to write off $5,250 per year per employee for tuition reimbursement plans under Section 127 of the Internal Revenue Code. This limit remains $5,250 for 2025.

Parents paying $5,250 in after-tax money to a college are using dollars that were subject to their 37% personal tax rate. It costs them $5,250 / (1 – 0.37) = $8,333 in pre-tax money to make that $5,250 college payment.

If they reimbursed their student via the tuition reimbursement plan, the business sees a deduction at the business tax rate (which often matches the top personal rate). The actual cost for the business is $5,250 times (1 – 0.37) = $3,307.50 to reimburse $5,250 of tuition—a huge savings!

Take note: the tax-free tuition reimbursement under Section 127 is only available to the employee (your student). Taking advantage of this plan may have to wait until the junior or senior years of college or graduate school, as the student must be 21, unless they are filing tax independent.

The above example is taking advantage of Section 127 of the Internal Revenue Code and comes with dollar limits and administrative requirements for employers. The benefit must be offered to all employees. A written plan must be in place. However, the education does not have to be job-related.

Section 132, Working Condition Fringe Benefit

An alternative option is under Section 132: Working Condition Fringe Benefit. Section 132 does not have dollar limits and does not have to be offered to all employees. A written plan is not required (although it is a good idea). Benefits can include travel expenses. However, the education must be job-related. The government may closely examine whether a college course is related to the employee’s current job. Section 132 may be a better idea for your business.

⚠️ A Caution to All Readers…

At Capstone, we are not tax professionals; we are Certified Financial Planners™. We wrote this to provide you with examples of how to tie everything together to maximize your savings. Careful due diligence, considering your family and business situation, will help identify which strategies and tactics are best suited to your overall financial plan.

Tax professionals file taxes for you. However, often they are not planners and may not suggest these types of strategies above. Financial “planners” are planning for the future, whereas accountants are “accounting” for the past. Tax “planning” is what produces results in the form of tax savings. Your tax professional will be more than happy to help you implement them and get all the i’s dotted and t’s crossed. You will need a tax professional, and we will work closely with them to help you make and implement a plan. We just want you to see the possibilities!

We believe strongly in leaving no stone unturned, and hope to show you the possibilities and how things can be different through college planning with tax strategies.

Get your tax savings optimized to CUT THE COST OF COLLEGE! Schedule a FREE consultation with us today.