When it rains, it pours! This week the Obama administration announced not only a new College Scorecard website but also revisions to FAFSA—both with the aim of making college more accessible to everyone. What is important for YOU to know to be an informed consumer of higher education?

First the College Scorecard…

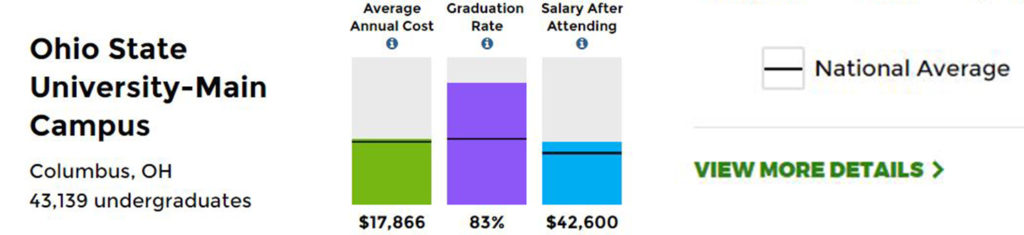

The Department of Education’s new College Scorecard website should provide families with increased transparency: true costs for each college, college’s success/graduation rate, and post-graduation salary. You can search by program, location, size, and specific name as well as other categories. Here’s an example from Ohio State’s Main Campus:

Some points to be aware of:

- All three categories displayed are the numbers for financial aid students. These numbers will be different for a family who does NOT qualify for need-based aid.

- The “graduation rate” is after 6 years—not 4.

- The “salary after attending” is 10 years after graduation.

Click on the “view more details” link to find additional information including:

- Costs for families in all salary ranges

- Typical total student loan debt after graduation

- Diversity and number of students

- ACT/SAT test scores ranges

- Most popular programs

The website is a good starting point for general data about your favorite colleges but proceed with caution. They are reporting average figures to give you a ball park cost of attendance, salary, etc. from those students who were awarded federal aid. Your scholastic achievement, family finances, and choice of major will dramatically impact what your “net cost” will be to attend each institution as well as your future earning potential. Dig deeper into each school you are interested in by going to the school’s Net Cost Estimator and research your future career earning potential on sites like Payscale.com and organizations like the National Association of Colleges & Employers for a complete picture.

Now the FAFSA…

The changes to the Free Application for Student Aid (FAFSA) are not as easy to understand. Currently seniors are applying to college in the fall and applying for the FAFSA starting in January AFTER they have already submitted college applications. The biggest change starting in October 2016 is students can file the FAFSA starting October 1st using the tax returns from the previous year. (Note this change does not affect the current seniors, the 2016 high school graduating class. This change impacts the high school graduating class of 2017 and anyone applying for financial aid for the 2017-18 school year and beyond.)

The changes will look like this…

| Seniors NOW 2015/2016 | Seniors 2016/2017 | |

|---|---|---|

| College Applications | Fall 2015 | Fall 2016 |

| FAFSA Available | January 2016 | October 2016 |

| Tax Year Figures Used | 2015 | 2015 |

Making this change is meant to make the process easier for families. Theoretically by moving up the date, you can have a clearer financial picture when selecting colleges to apply to. Also when families complete the FAFSA now they commonly have to use estimated tax numbers and then revise the FAFSA with actual numbers afterwards. The 2016 plan will eliminate the need to revise your numbers. You will use the actual returns you have already submitted for the prior year.

At Capstone, we are all about proactive planning to create an ideal outcome for you and your students! Don’t wait until fall of your student’s senior year. It will be too late!

Our 3 proactive points…

- Financial aid and tax aid planning for college need to begin freshmen year of high school. The most important planning year will now be the spring of your sophomore year and the fall of your junior year. This period will be the tax year used on the FAFSA as your “base year”. Why is that year so important? Your financial aid filing for your college freshmen year is what we call your “base year”. Your base year is critical as colleges frequently award the most aid to incoming freshmen, and often the aid is in 4-year renewable scholarships. You still need to fill out the FAFSA each year, but you want to look as poor as possible in your freshmen year, as it forms the basis of your financial aid package for all four years.

- Use an EFC estimator and the Net Cost Calculator on each college’s website in your high school junior year at the latest so parents and students can have a conversation about realistically affordable colleges.

- Create a comprehensive 4-year college funding strategy incorporating college selection, financial aid, asset and income tax strategies, and a plan to minimize your student’s debt.

Future FAFSA changes meant to simplify the questions and streamline the process are constantly under discussion. In the meantime, take matters into your own hands by having a plan. Know your pre-approval amount and ensure your student graduates on time with manageable student loan debt without robbing mom and dad’s retirement!